The software streamlines the process a bit, compared to using spreadsheets. But you’re still 100% on the line for making sure those adjusting entries are accurate and completed on time. Making adjusting entries is a way to stick to the matching principle—a principle in accounting that says expenses should be recorded in the same accounting period as revenue related to that expense. Non-cash expenses – Adjusting journal entries are also used to record paper expenses like depreciation, amortization, and depletion. These expenses are often recorded at the end of period because they are usually calculated on a period basis.

- In this article, we shall first discuss the purpose of adjusting entries and then explain the method of their preparation with the help of some examples.

- Adjusting journal entries can also refer to financial reporting that corrects a mistake made earlier in the accounting period.

- If your business uses the cash basis method, there’s no need for adjusting entries.

- In some situations it is just an unethical stretch of the truth easy enough to do because of the estimates made in adjusting entries.

- Check out this article “Encourage General Ledger Efficiency” from the Journal of Accountancy that discusses some strategies to improve general ledger efficiency.

Types of Adjusting Entries

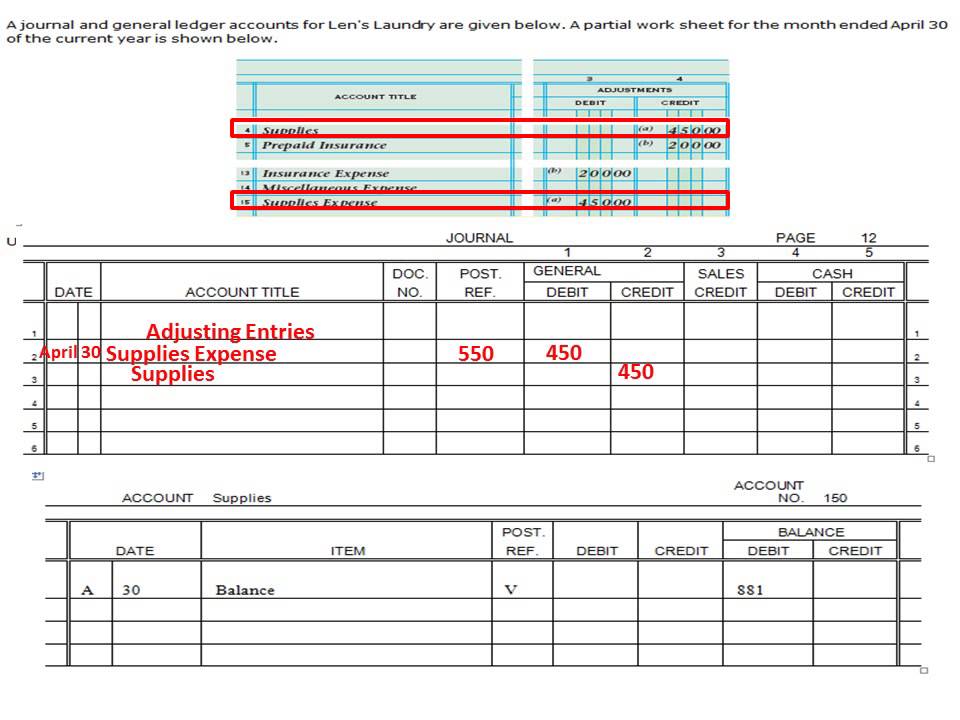

The process of recording such transactions in the books is known as making adjustments. An adjustment can also be defined as making a correct record of a transaction that has not been entered, or which has been recorded in an incomplete or incorrect way. Estimates are adjusting entries that record non-cash items, such as depreciation expense, allowance for doubtful accounts, or the inventory obsolescence reserve. In summary, adjusting journal entries are most commonly accruals, deferrals, and estimates.

Link to Learning

Once all adjusting journal entries have been posted to T-accounts, we can check to make sure the accounting equation remains balanced. Following is a summary showing the T-accounts for Printing Plus including adjusting entries. For example, if you place an online order in September and that item does not arrive until October, the company you ordered from would record the cost of that item as unearned revenue.

How much will you need each month during retirement?

You must calculate the amounts for the adjusting entries and designate which account will be debited and which will be credited. Once you have completed the adjusting entries in all the appropriate accounts, you must enter them into your company’s general ledger. A business may earn revenue from selling a good or service during one accounting period, but not invoice the client or receive payment until a future accounting period.

11 Financial may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. 11 Financial’s website is limited to the dissemination of general information pertaining to its advisory services, together with access to additional investment-related information, publications, and links. Students should carefully note that every adjustment has at least two effects due to double entry. If the Final Accounts are prepared without considering these items, the trading results (i.e., gross profit and net profit) will be incorrect.

Adjusting Entry for Prepaid Expense

It means that for this part, the supplier has received only a part of the amount due to him/her. In such cases, therefore an overdraft would be created in his books of accounts and he will have to adjust it when he receives the balance by making an adjusting entry. The accrual accounting convention demands that the right to receive cash and how invoice financing works the obligation to pay cash must be accounted for. This necessitates that adjusting entries are passed through the general journal. Therefore, it is considered essential that only those items of expenses, losses, incomes, and gains should be included in the Trading and Profit and Loss Account relating to the current accounting period.

This systematic allocation helps in presenting a more accurate financial position by gradually reducing the asset’s book value. Depreciation methods can vary, with straight-line and declining balance being the most common. The choice of method can impact the financial statements and tax liabilities. Since the firm is set to release its year-end financial statements in January, an adjusting entry is needed to reflect the accrued interest expense for December.

No matter what type of accounting you use, if you have a bookkeeper, they’ll handle any and all adjusting entries for you. If you do your own accounting, and you use the accrual system of accounting, you’ll need to make your own adjusting entries. To make an adjusting entry, you don’t literally go back and change a journal entry—there’s no eraser or delete key involved.